The last year has been an interesting time for the Chinese mobile games market, especially as the global COVID pandemic has impacted how people are playing games. We’ve conducted a year-on-year revenue analysis of iOS games in the Chinese mobile games market between Q2 2019 and Q2 2020 to see what the most significant changes have been in the space of a year. Looking at the market from the perspective of market share, revenues and mobile game design we’ve analysed what the most significant markets shifts were as well as which game categories, genres or publishers best capitalised on this market opportunity. We’ve also taken a look at the different mobile game sub-genres to see if any of them have seen significant changes in their momentum. Here’s what we found.

Editor’s Note: This article was originally published in pocketgamer.biz. For more insights on mobile gaming market development in major markets check out these posts on the US and Japan respectively.

(Note: All data in this post is based on IAP revenues from iOS China top 500 games. “Rev” indicating revenue in Q2 2020, “MS” indicating Revenue Market Share in Q2 2020, “change” indicating the YoY difference between Q2 2020 and Q2 2019. All currency is in $USD. Market Share percentages reflect the category/genre/subgenre/publisher’s position in relation to other categories/genres/subgenres/publishers. For a full explanation of the genre taxonomies referred in this analysis, please see here)

China Mobile Games Market Overview – Subgenres

Key Takeaways:

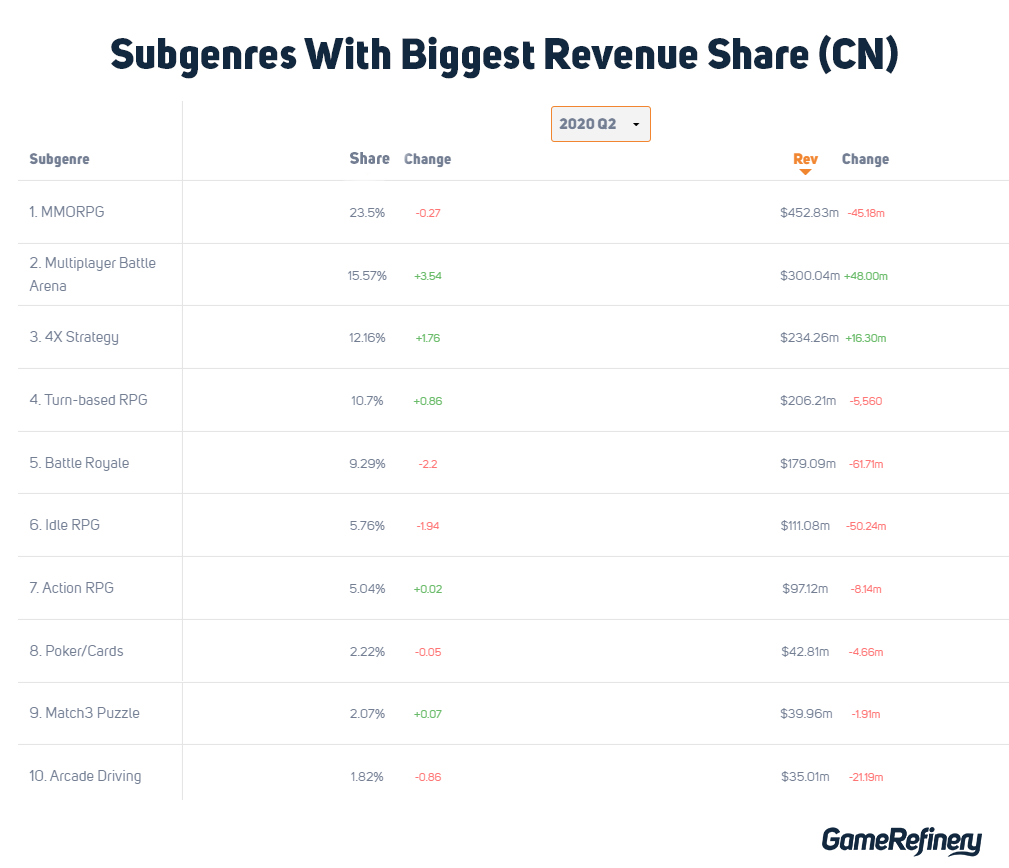

- The top loser for quarterly revenue share across all subgenres in the China iOS market was the MMORPG one which has long been a healthy staple of Chinese gamers. The MMORPG genre dropped over eight per cent during the year down to 23.5% out of all game revenues. This is still a very respectable number, but the drop translates to almost $108 million, leaving the MMORPG subgenre at over 452 million USD in revenue in Q2 2020.

- Other subgenres that took a hit include AR and Platformer, both primarily supported by single titles (Let’s Hunt Monsters and Ninja Must Die 3).

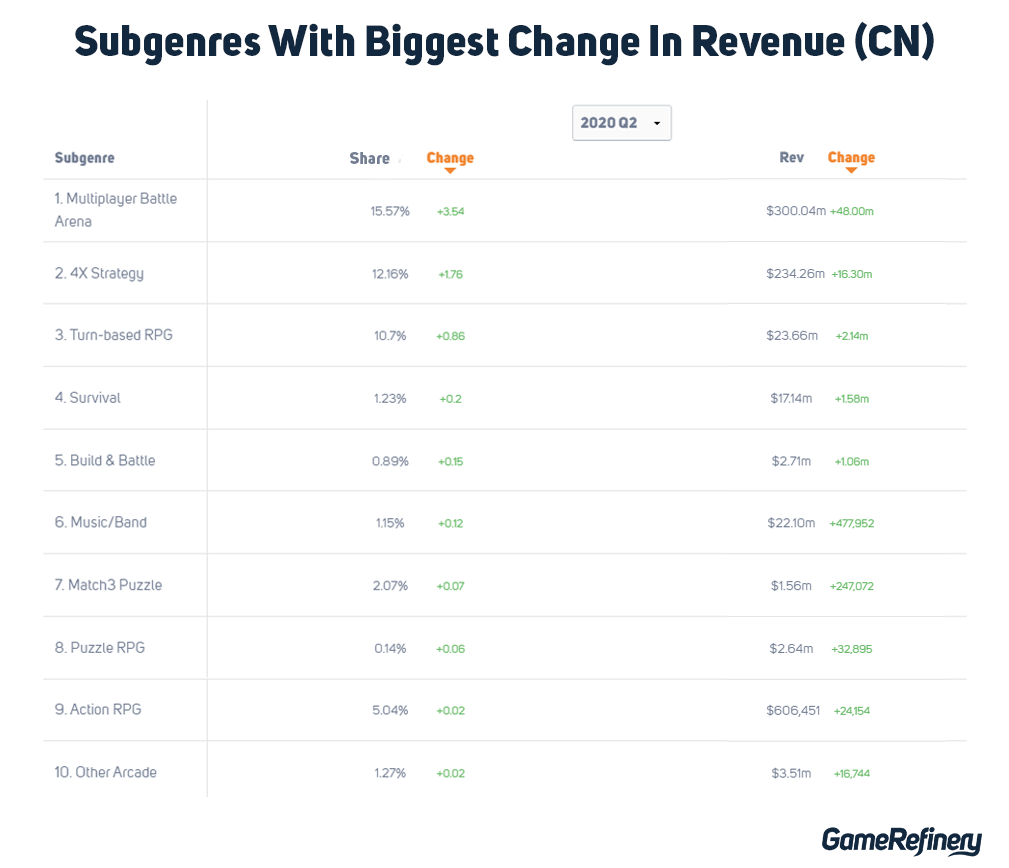

- On the positive side, these were good times for other Mid-Core genres such as 4X Strategy (Game of War-like city builders) and Battle Royale as well as MOBAs and Idle RPGs.

- The growth of the 4X Strategy subgenre can mostly be attributed to Lingxi Games’ “Romance of the Three Kingdoms – Strategic version” (三国志·战略版), which has been a big hit since late 2019

- The growth of Battle Royale is almost entirely caused by the continued success of Tencent’s PUBG Mobile, while the big leap in the Idle RPG genre is mostly thanks to Lilith Games’ AFK Arena.

- An interesting phenomenon we’ve noticed is the growth of the Poker/Cards subgenre, which has previously been marginal in China. Poker/Cards grew in terms of market share and revenues from 1.6% and 28m$ to 2.2% and 43m$. This growth can likely be linked to real-life mahjong parties being banned in some parts of China due to the pandemic.

Top publishers in the Chinese mobile games market- Key Differences

Key Takeaways:

- A year ago (Q2 2019), Tencent still held 49.58% of the Chinese iOS game market revenue. A year later, Tencent’s share of the market’s revenue had dropped to 39.26%, meaning a decrease of over $125 million in quarterly revenue in Q2 2020 compared to the year before. Tencent’s market share has reduced by 10%, making it the only top 10 market share publisher not seeing revenue growth.

- During the same period, Tencent’s old rival and biggest competitor NetEase, also saw a slight decrease in its share of game revenue in the Chinese iOS market, falling from 17.82% to 16.84%. However, there was no drop in quarterly revenue value. On the contrary, NetEase’s quarterly revenue in Q2 2020 saw a slight increase of almost $7.5 million compared to the year before.

- This change in the standing of both giants (Tencent and NetEase) can likely be explained with the influx of new publishers that have been able to grab their share of the Chinese iOS market. The number one grower of these studios was Alibaba Group’s Lingxi Games, which grew from a tiny 0.38% market share in Q2 of 2019 to a notable 6.64% in Q2 of 2020. This translates into a growth of over $121 million in quarterly revenue compared to a year before. In second place was Lilith Games Shanghai, which saw its market share grow from zero to 2.89%, or $55 million in quarterly revenue, all thanks to its hit game AFK Arena.

In Conclusion

From our analysis of the Chinese mobile games market (iOS) from 2019 to 2020, we can conclude the following:

Subgenres:

- The MMORPG subgenre endured a significant loss in terms of market share and revenues.

- Respectively, other Mid-Core subgenres were able to increase their market share, including 4X Strategy, Idle RPG and Battle Royale games.

- Poker/Cards excellent performance is an interesting phenomenon likely due to the pandemic.

Publishers:

- Tencent suffered a notable hit to its market share and revenues.

- Lingxi Games was one of the major publishers to grow in market share with games such as Sanguozhi.

- Lilith Shanghai was also able to scale up its market share from 0% to 2.9% thanks to AFK Arena’s launch in China.

Want to see Market Share live in action? Get in touch with us here.

If you enjoyed reading this post, here are a few more you should definitely check out: